Other2025-10-11

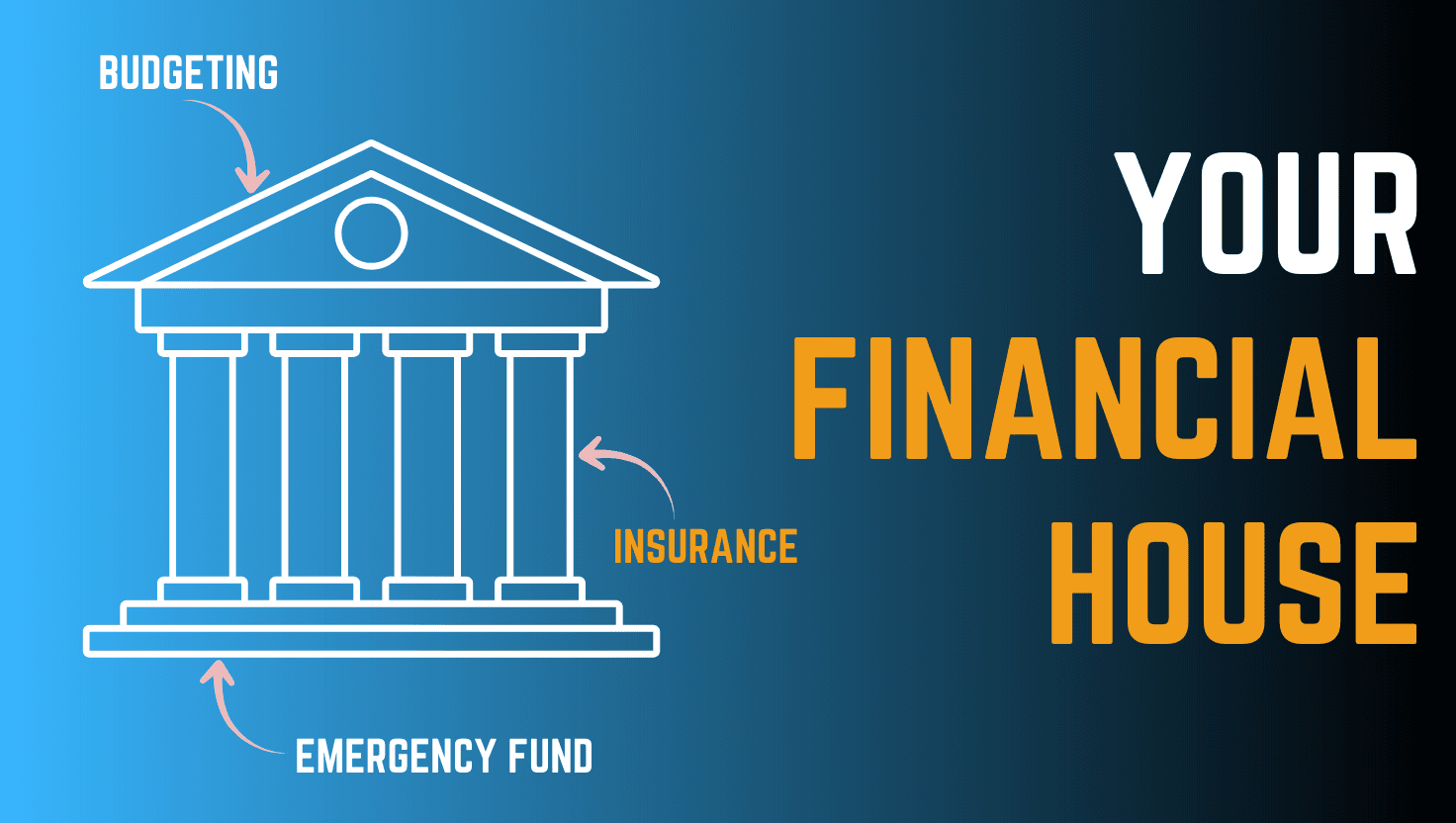

Your Financial House: The 3 Basics (Emergency fund, Insurance, Budget)

Imagine your financial life as a sturdy house. No builder would skip a strong foundation, support pillars, or a reliable roof. Likewise, for personal finance fo...